With Qualcomm's acquisition of NXP, Intel introduced a variety of car gauge processors, MediaTek's follow-up, automotive electronics is undoubtedly the next gold mining company to explore, but how is the global automotive electronics industry changing? What position does China play in it? Let's take a closer look.

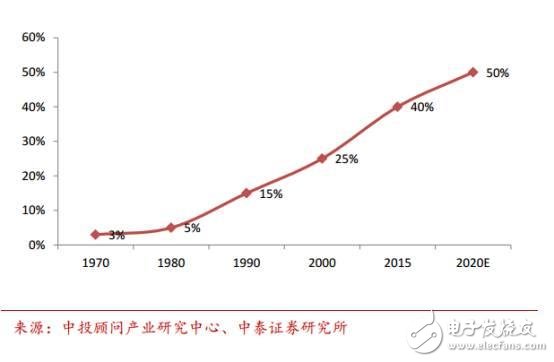

Electrification and intelligence provide new growth points for automotive electronicsThe automotive electronics industry continues to expand as consumers' demand for vehicles increases, the use of networks in vehicles, increased safety requirements, the transition between mechanical and electronic systems, and the performance of powertrains. In 2014, the total scale of China's automotive electronics market reached 384.4 billion yuan, and CAGR reached 21% in the past 5 years; the proportion of automotive electronics products in total vehicle costs continued to increase, from 5% in the late 1980s to 25% today. More than 30% of mid-to-high-end cars are expected to have a value of 50% in high-end cars.

China's automotive electronics market scale (100 million yuan)

Classification of automotive electronics

Automobile electronic vehicle cost ratio

But we also need to understand a status quo. The current automotive electronics market is basically the world in Europe, America and Japan. The local enterprises in China's automotive electronics market are mostly concentrated in the low-end market, and they are mostly concentrated in the aftermarket, and there are fewer enterprises.

Multinational companies dominate the mid- to high-end market, and 20% of foreign-invested companies have a market share of nearly 70%. There are more than 2,400 local enterprises, and less than 20 have a revenue of more than 1 billion yuan. The matching rate of local enterprises in the domestic independent brand vehicle has increased, and it has begun to penetrate into the mid-range automobile. For example, the high-intensity lamp rectifier controller, vehicle terminal and airbag lamp have been cut into the mid-range automobile supporting system.

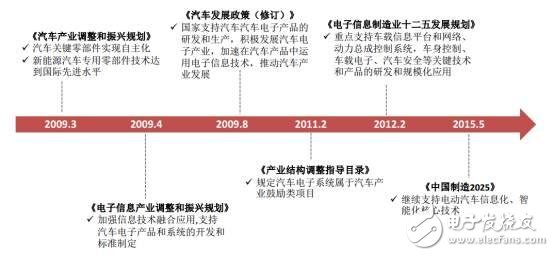

In order to promote the development of China's automotive electronics industry, the state has introduced a series of policies.

National promotion of automotive electronics development policy summary

Analysis of the Status Quo of Automotive Electronics LocalizationAlthough the high-end market is occupied by Europe and the United States, it is undeniable that in recent years, China's automotive electronics industry has also made great progress. In some areas, breakthroughs have been made, and the traditional power control system is now more localized and has fewer growth points. At present, in addition to automotive pressure sensors, flow sensors and other key components still rely on imports, the power control system has basically completed localization or has been partially localized. At present, the penetration rate of traditional automobile power systems is high and the growth point is small.

Engine electronic control unit system

Power control class automotive electronic classification and localization process

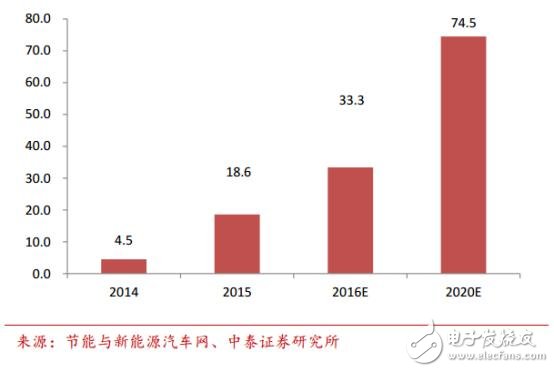

Especially worth mentioning here is the development of China's BMS industry.Benefiting from the rapid growth of electric vehicles, the BMS industry will reach 7.5 billion yuan in 2020. In 2015, the output of new energy vehicles was 330,000, and the penetration rate reached 1.35%, entering the high-speed growth period. According to the BMS unit price of 0.3 million yuan for passenger cars, 10,000 yuan for passenger cars and 0.5 million yuan for special vehicles, the output value of new energy vehicle BMS market in 2015 was about 1.86 billion yuan.

Assume that the sales volume of passenger cars, buses and special vehicles will be 28 million, 500,000 and 1.5 million in 2020. The penetration rate will reach 5%, 50% and 10% respectively. In 2020, the BMS market will reach 7.5 billion yuan. CAGR Reached 32%.

China's BMS market size

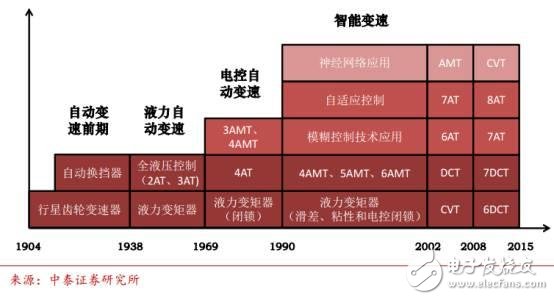

Another thing to mention is the automatic transmission, China will usher in new opportunities.

We know that there are many applications for the chassis control system of the car. Applications such as lane keeping and electronically controlled suspensions are constantly appearing, but the popularity is long and the market growth is slow in the future.

Chassis control system classification and localization process

However, the low automatic transmission rate of the automatic transmission is the focus of future industrialization.

At present, the sales of automatic transmission models have been more than half, but the annual matching capacity of passenger auto-automatic transmissions is less than 5%. In addition, due to the lack of development of bearings and oil seals for some core components, automatic transmissions still have a gap in quality stability and reliability with imported and joint venture transmissions.

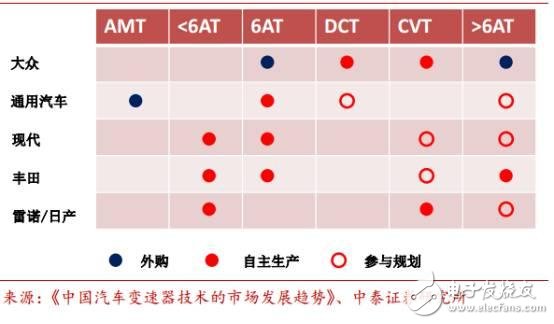

The automatic transmission industry is highly valued, and the "Automotive Industry Adjustment and Revitalization Plan" clearly supports the development of commercial vehicles AMT, six-speed manual and automatic transmission (AT), dual clutch automatic transmission (DCT) and continuously variable transmission (CVT). technology.

Foreign manufacturers transmission technology route

The automatic transmission ushered in the opportunity of technological upgrading, and 6AT, CVT and DCT are the main growth points in the Chinese market. Whether it is a traditional manual transmission or a fast-developing automatic transmission, there will be opportunities for technological upgrades in the next five years.

(1) AT products enter the stage of independent innovation, and 6AT will become mainstream. In the traditional gear transmission field, 6AT has quickly replaced 4AT as the mainstream of the market, and the advanced 8/9AT has emerged, and will become the standard configuration for high-end models in the future.

(2) DCT products entered the initial stage of industrialization. A number of independent car companies have planned independent DCT. Among them, SAIC, BYD, GAC and JAC's independent DCT models have been on the market, and Changan and Geely's DCT will be mass-produced this year. In addition, DCT is similar to the MT industry and is easier to industrialize.

(3) CVT products entered the initial stage of industrialization. CVT transmissions already have their own technology. Chery and Rongda CVT have achieved mass production.

(4) AMT is industrialized in the commercial vehicle market. The AMT shifting logic is unclear, has a strong sense of frustration, and has a poor driving experience. It has gradually been phased out by the passenger car market and is now industrialized in the commercial vehicle market.

Automatic transmission technology development history

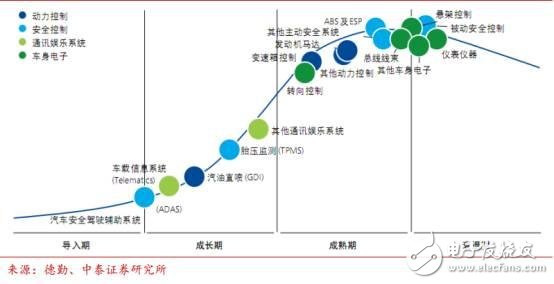

Smart car drives, ADAS, in-vehicle systems, TPMS grow at a high speedWith the development of automotive intelligence, the requirements for active safety, communication and navigation, visual technology, identification technology, infotainment, comfort and environmental protection have all been improved. The demand for safety control and automotive electronics applications will be greatly enhanced.

Automotive electronics technology in the era of smart car

ADAS, in-vehicle information systems, and tire pressure detection systems (TPMS) enter the high-speed growth period. From the perspective of the life cycle of automotive electronics, ADAS, in-vehicle information systems, and tire pressure monitoring systems will enter the growth phase.

(1) Vehicle intelligentization One path is the intelligentization of bicycles, and ADAS is the basis for implementation. As the sales of ADAS expands, ADAS products will also enter the local production stage.

(2) Another path of automobile intelligence is the interconnection between vehicles and vehicles, vehicles and roads, vehicles and networks, and vehicles and people. The so-called vehicle networking is mainly realized by in-vehicle information systems. With the development of the mobile Internet and the integration of Internet companies, the industry will enter an outbreak period.

(2) In the "Performance Requirements and Test Methods for Passenger Car Tire Pressure Monitoring System" promulgated this year, the tire pressure monitoring system will become the national mandatory equipment for the future delivery of new cars.

Automotive electronics market segment life cycle

Grasping the opportunities of localization under technological upgradingIn the big environment of automobile transformation, China can start to improve its technical level from many aspects. The first is BMS.

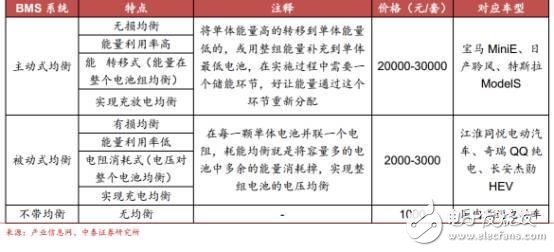

The technical requirements of domestic car companies for BMS will increase, and the market will face tremendous opportunities and challenges. At present, BMS products prevalent in foreign countries mostly adopt active equalization function design. Most of the mainstream electric vehicles in the world adopt the active equalization mode, but the price of this product is relatively high.

The domestically adopted passive equalization function and BMS products without equalization function are low in price and simple in function. In the future, with the large-scale production of electric vehicles, the technical requirements of domestic vehicle manufacturers for battery management systems will inevitably increase, and the development of battery management system (BMS) market faces enormous opportunities and challenges.

The level of the BMS system and the corresponding models

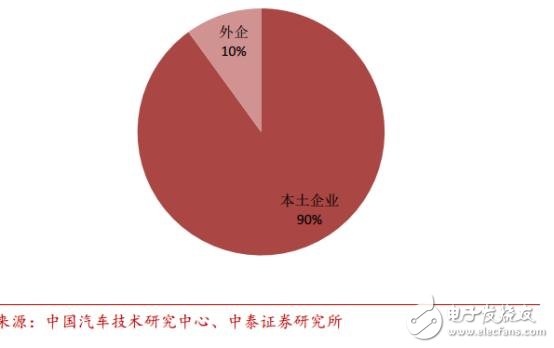

Now, China's BMS market is dominated by local manufacturers.

The BMS suppliers used in pure electric passenger cars produced in China present four types: professional BMS manufacturers, OEMs, battery manufacturers, and integrated auto parts companies. Among them, the BMS installed by the OEM has accounted for about 28% of the total. The BMS installed by the battery plant has a share of about 12%, and the professional BMS manufacturers account for about 60%. From the nature of BMS suppliers, foreign companies account for about 10%, local companies account for about 90%, and local manufacturers dominate.

2015 China Pure Mobile Passenger Car BMS Market Share

However, we also understand that the BMS core technology threshold is high, and professional manufacturers have the advantage of data accumulation. The three core functions of BMS are cell monitoring, state of charge (SOC) estimation and cell balancing.

SOC and battery balancing technology are technically difficult and require a large amount of BMS operational data to be accumulated, while professional BMS manufacturers have an advantage. The professional representative enterprises include Junsheng Electronics, Huizhou Yineng, Anhui Ligao, Shenzhen Ke Lie Technology, Shenzhen Guoxin Power, and Hangzhou Energy Saving Power. The main engine factory mainly supports its own new energy vehicles. The representative enterprises include BYD, Condit, and Changan New Energy. Representatives of battery factories include CATL, Waterma, Pride, and Xinwanda.

In addition, automatic transmissions are also opportunities in localization and capacity growth.As domestic demand for DCT transmissions and CVT transmissions increases, the capacity of automatic transmission manufacturers will continue to increase in the coming years. According to the IHS powertrain estimates, by 2020, about 30 large-scale automatic transmission projects will be put into production or capacity upgrades in China. According to statistics, the total amount of domestic DCT, CVT, and AT will expand from 3.76 million units in 2014 to 11.11 million units in 2020.

National Automatic Transmission Manufacturer Distribution and Capacity Planning (2014→2020)

In addition, under the impetus of intelligent car and unmanned driving, millimeter wave radar, chip algorithm, intelligent terminal and TSP are new points of view.

The first is that ADAS has entered the stage of localized production, with a market size of 18 billion yuan in five years. As the sales of ADAS expands, ADAS products will also enter the local production stage. According to SBD estimates, the size of China's ADAS market in 2014 was 540 million euros (about 4 billion yuan). By 2021, the market size reached 2.5 billion euros (about 18 billion yuan) and CAGR reached 24%.

The cost of laser radar for ADAS is high, the threshold of ultrasonic radar is low, and the millimeter wave radar is expected to be quickly localized.

The radars in ADAS are now mainly divided into laser radar, ultrasonic radar and millimeter wave radar. Due to the high cost and lack of commercialization of laser radar, the ultrasonic radar technology has low thresholds and many suppliers, and the cost of millimeter wave radar is between the two. Although the technology is mainly in the hands of TRW, Bosch, mainland and other companies, it is expected to be realized first. Localization.

Millimeter wave radar technology is relatively mature, and the price is not out of reach. In the next two years, a large number of millimeter wave radar products will be launched, and the price will drop rapidly, which will promote the large-scale application of millimeter wave radar in collision avoidance and ranging.

Domestic algorithm companies have strong R&D capabilities and focus on potential leading companies. At present, domestic algorithm companies mainly have specialized algorithm companies as well as TIE1 suppliers and vehicle companies. The former has accumulated many years in the field of vision, has strong competitiveness in algorithms, and has been able to basically realize the functions of ADAS. There is not much difference between Mobileye and the key indicators such as vehicle recognition rate.

Localization process of millimeter wave radar

The main domestic ADAS algorithm company

The Internet of Vehicles will also be the focus of attention.The popularity of the Internet has made the mobile phone model an important way to realize the Internet of Vehicles. Internet companies have rich Internet resources and strong basic support, and they appear as industrial chain integrators.

According to SBD estimates, China's car-connected terminals will grow from less than 1 million units in 2013 to 10 million units in 2018, an increase of nearly 10 times. The mobile phone-car model will quickly spread to mid- to low-end models.

According to staTIsta's forecast, the 15-year Internet of Vehicles market is US$5.04 billion (approximately RMB 33 billion), and the market size is expected to reach US$33.82 billion (approximately RMB 220 billion) by 2020. The penetration rate of China's Internet of Vehicles increased from 4.8% in 16 years to 18.1% in 2020; the number of Internet-connected users reached 44.1 million by 2020. The overall industrial chain maintained rapid growth.

China's car networking market size

We should also see that in this field, the pre-installation market is still the main and post-installation market is more likely to break out, focusing on the potential leader with core technology.

1) In the pre-installation market, because the car factory controls the hardware entrance of the car, it has a high entry threshold and is subject to many restrictions. The post-installation market, with its low-cost, easy-to-assemble advantages, the potential for mobile Internet development brings a huge amount of potential to use the car-networking service through the mobile-car model.

2) The current post-installation vehicle terminal product features and services are less differentiated and have fewer innovative products. In addition to basic functions such as vehicle detection and driving habit tracking, intelligent in-vehicle terminals must have a series of features that enhance user stickiness and innovative applications to stand out from the crowd.

China vehicle network front and rear installed terminal scale (10,000 units)

On the TSP platform, the aftermarket is open and easier to cut.

(1) The Internet of Vehicles operators directly provide services to consumers, distribute profits, and play the role of data entry. They are at the core of the industry chain and have huge potential profit margins.

(2) After the market, the difficulty of cutting is relatively low and the entrance is open. The localization threshold is high, focusing on online and offline resource-rich enterprises.

Scale of car networking services

Furthermore, the development of electronic control system software faces time window opportunities.

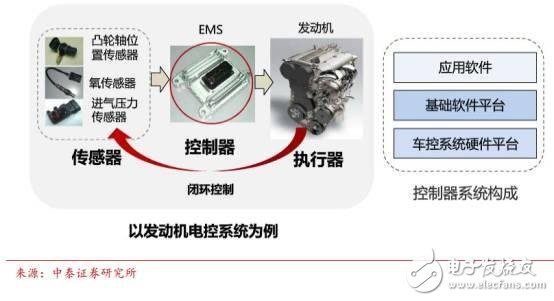

The electronic control system software is the core of the automotive electronic control system. The electronic control system of a car generally consists of three parts: a sensor, a control unit and an actuator.

1) The sensor converts the external operation signal, the status signal of the car, the driver's operation signal, etc. into an electrical signal, and sends it to the electronic control unit.

2) The electronic control unit processes the input signal and generates a corresponding control signal.

3) The actuator receives the control signal output from the electronic control unit and outputs the corresponding physical quantity to control the car.

Anatomy of the electronic control system

New technologies have enabled automotive infrastructure software to usher in the development of time window opportunities. Under the trend of vehicle platformization, component generalization and electronic function, the role of automotive basic software in automotive electronic systems is highlighted. The impact of new technologies on traditional technologies has led to the development of domestic automotive electronics infrastructure software.

Evolution of automotive electronic control technology system

The domestic automotive electronic control system software is nearly 10 billion yuan, and it is urgent to serve the industry as a specialized enterprise.

1) According to the average software accounting for 5% of the cost of each electronic control system, the software of the electronic control system in the self-owned brand passenger car is close to 1 billion yuan. If it is extended to commercial vehicles and joint venture vehicles, the domestic electronic control system software can reach 10 billion yuan.

2) In the current industry chain, when using foreign parts, basic software and chips, independent software vendors are just starting out and lacking independent chips. Specialized enterprises that need to be effectively satisfied and need to serve the industry.

China's automotive electronic control system software company

Although China's automotive electronics has made significant progress in recent years, we also need to understand that in the high-end field, it is basically the world of foreign manufacturers, especially in the chip field, which is almost difficult for Chinese manufacturers. The restricted area of ​​the enterprise. However, in recent years, with the efforts of manufacturers such as Quanzhi, China's front-loading chips have also made a good breakthrough. Looking ahead, China's automotive electronics will get a bigger leap.

Representative company of the international automobile industry chain

Round Tapered pole are furnished with anchor bolts featuring zinc-plated double nuts and washers. Galvanized anchor bolts are optional.

Yixing Futao Metal Structural Unit Co. Ltd. is com manded of Jiangsu Futao Group.

Round Taper Steel Pole, Round Taper Galvanized Steel Pole,Round Tapered Pole

YIXING FUTAO METAL STRUCTURAL UNIT CO.,LTD( YIXING HONGSHENGYUAN ELECTRIC POWER FACILITIES CO.,LTD.) , https://www.chinasteelpole.com